(2)")

In a recent Judgement of Delhi High Court In Sarita Bakshi Vs. State the Hon’ble High Court first evaluated the salary slip of the Husband which looked like as mentioned below..

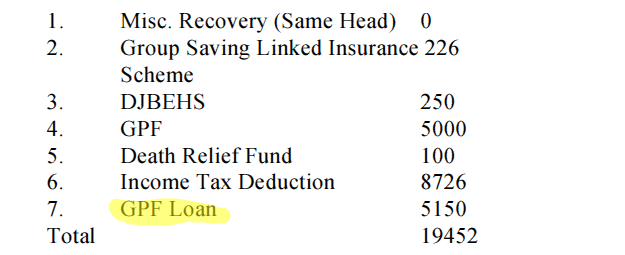

The Husband has deliberately shown a GPF loan deduction of Rs. 5150 which is deducted from salary but court held in this Judgement as under

In the present case, the total of income of the respondent has been shown as Rs. 49,407/- and the deductions have been shown as Rs. 19,452/-. After deductions the net carry on salary will come to Rs. 29,955/-. The learned Trial Court has rightly held that the deduction of Rs. 5,000/- towards recently taken personal loan cannot be considered as deduction as it is for his personal benefit and not mandatory statutory deduction; the total carry on home salary will thus come to about Rs. 35,000/- per month.

- The Apex Court in the matter of Kulbhushan Kumar vs. Raj Kumari and Others MANU/SC/0349/1970 : (1970) 3 SCC 129 while adjudicating the deductions that can be made from the income of the husband before awarding maintenance, observed as below:

“…19. It was further argued before us that the High Court went wrong in allowing maintenance at 25% of the income of the appellant as found by the Income-tax Department assessment proceedings under the Income-tax Act. It was contended that not only should a deduction be made of income-tax but also of house rent, electricity charges, the expenses for maintaining a car and the contribution out of salary to the provident fund of the appellant. In our view some of these deductions are not allowable for the purpose of assessment of “free income” as envisaged by the Judicial Committee. Income-tax would certainly be deductible and so would contributions to the provident fund which have to be made compulsorily. No deduction is permissible for payment of house rent or electricity charges. The expenses for maintaining the car for the purpose of appellant’s practice as a physician would be deductible only so far as allowed by the income-tax authorities i.e. in case the authorities found that it was necessary for the appellant to maintain a car…”

- A similar view was taken in the case of Nitin Sharma and Others vs. Sunita Sharma & Others (MANU/DE/0279/2021 : 2021 III AD (Delhi) 210), wherein a bench of this Hon’ble Court was pleased to hold as under:

“24. In the opinion of this Court, while calculating the quantum of maintenance, the income has to be ascertained keeping in mind that the deductions only towards income tax and compulsory contributions like GPF, EPF etc. are permitted and no deductions towards house rent, electric charges, repayment of loan, LIC payments etc. are permitted. On this aspect, the pertinent observations of Hon’ble Supreme Court in Dr. Kulbhushan Kunwar v. Raj Kumari MANU/SC/0349/1970 : (1970) 3 SCC 129, which have been followed by a Bench of Punjab & Haryana High Court in Seema & Anr. Vs. Gourav Juneja, are as under:-

“12. Section 125 Cr.P.C. stipulates that if any person having sufficient means neglects or refuses to maintain his wife, his legitimate or illegitimate minor child, who are otherwise unable to maintain themselves, shall be obligated to do so. A moral duty and a statutory obligation is cast upon the husband to maintain his wife, minor children, parents who otherwise are not capable of maintaining themselves. A person cannot be permitted to wriggle out of his statutory liability by way of availing huge loans and reducing a substantial amount of his salary for repayment of the same every month. Deductions that are made from the gross salary towards long term savings, which a person would get back at the end of his service and such as deductions towards Provident Fund, General Group Insurance Scheme, L.I.C. Premium, State Life Insurance can be deemed to be an asset that he is creating for himself. In arriving at the income of a party only involuntary deductions like income tax, provident fund contribution etc. are to be excluded. Therefore, such deductions cannot be deducted or excluded from his salary while computing his “means” to pay maintenance. In the case of Dr. Kulbhushan Kunwar v. Raj Kumari MANU/SC/0349/1970 : (1970) 3 SCC 129: 1971 AIR (SC) 234 while deciding the question of quantum of maintenance to be paid, the argument raised that deduction not only of income-tax but also of house rent, electricity charges, the expenses for maintaining a car and the contribution out of salary to the provident fund of the appellant was not allowed. Only deductions towards income-tax and contributions to provident fund which had to be made compulsorily were allowed. The relevant portion of Dr. Kulbhushan Kunwar’s case (supra) reads as under:–

“19. It was further argued before us that the High Court went wrong in allowing maintenance at 25% of the income of the appellant as found by the Income Tax Department in assessment proceedings under the Income Tax Act. It was contended that not only should a deduction be made of income-tax but also of house rent, electricity 20-11-2021 (Page 5 of 8) www.manupatra.com Ishaan Sharma charges, the expenses for maintaining a car and the contribution out of salary to the provident fund of the appellant. In our view some of these deductions are not allowed for the purpose of assessment of “free income” as envisaged by the Judicial Committee. Income Tax would certainly be deductible and so would contributions to the provident fund which have to be made compulsorily. No deduction is permissible for payment of house rent or electricity charges. The expenses for maintaining the car for the purpose of appellant’s practice as a physician would be deductible only so far as allowed by the income-tax authorities i.e. in case the authorities found that it was necessary for the appellant to maintain a car…”

- In a nutshell, a husband cannot be allowed to shirk his responsibility of paying maintenance to his wife, minor child, and parents by availing loans and paying EMIs thereon, which would lead to a reduction of his carry home salary”

Sarita Bakshi vs. State and Ors. (03.06.2022 – DELHC) : MANU/DE/2076/2022

However the court allowed that the father of the husband who is 79 Years old and dependent on Son as legitimate and considered his share to be deducted.

Also the share of divorce sister were also considered as a deduction.

The father of the respondent may not be present before the Court to ask for maintenance, there is no argument or proof of his being independent or having financial resources to maintain himself. This Court still has to appreciate that even though he has not appeared before this Court it cannot be denied that he has to depend on his son at the age of 79. The father may not have considered filing case for maintenance before a Court of law. At times, parents may feel sad and inferior even at the thought of being maintained by their child and asking for maintenance. Their love and affection for their child is so overpowering that they may decide to live uncomfortably but not ask for maintenance. Parents want to feel independent as they don’t live with their children, their children live with them. With these thoughts in mind, I hold that the needs of the father are not many as he is staying with the respondent but a certain amount of expenditure must be apportioned for his needs.

In the present case, the learned counsel for the petitioner contends that a divorced sister cannot be held to be dependent on the petitioner. In my opinion, this stand is meritless to the extent that in India, the bond between siblings and their dependence on each other may not always be financial but it is expected that a brother or sister will not abandon or neglect his or her sibling in time of need. I completely agree with the learned counsel for the respondent that the petitioner’s divorced sister for claim for her maintenance and dependence can file a case against her husband. However, it has not been made clear in the present case as to whether the divorced sister of the respondent is receiving any maintenance or is being maintained by her husband or not. It is also not clear as to whether she is able to maintain herself as no argument has been put forth before this Court and it also does not find any mention in the judgment of the learned Trial Court. Therefore, I am of the view that though the divorced sister can legally and morally claim maintenance from her husband, the respondent, at the same time, must be spending and is expected to spend some amount for his sister on special occasions and in case of any emergent need. Therefore, though while apportioning the income of the respondent, one portion of income of the respondent cannot be apportioned to the sister, some amount as expenditure on yearly basis has to be kept aside for the divorced sister as moral obligation of the respondent. The plea of the petitioner that no amount should be considered to be spent on the divorced sister is meritless especially in the Indian context and the peculiar circumstances of the present case.

Sarita Bakshi vs. State and Ors. (03.06.2022 – DELHC) : MANU/DE/2076/2022

Advocate Nitish Banka is a first-generation lawyer with over a decade of courtroom experience, known for his strategic defense in complex matrimonial and criminal litigation. He is the founder of Lexspeak Legal, a premium litigation practice that focuses on false 498A/DV cases, maintenance disputes, quashing petitions, discharge, counter-cases, and high-stakes matrimonial strategy for Indian and NRI clients.

connect on 9891549997

Widely recognised for simplifying complex legal processes

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Our deepest appreciation goes to bloggers who consistently provide quality content. Their informative, honest, and inspiring writing greatly helps readers broaden their horizons. The dedication, creativity, and hard work of bloggers have a positive impact and make blogs a trusted and useful source of information for many.